Every year, plenty of companies treat the annual report like a fire drill. The deadline is known months in advance, yet the final weeks turn into a scramble of missing data, last-minute edits, and a designer waiting on copy that keeps changing.

It does not have to work that way. A good annual report is not something you write in a rush at year-end. It is the output of a long, ordered process that runs across several teams, each picking up the work at the right moment.

Before we walk through how a report is built, it helps to be clear on what an annual report actually is, the two formats you can choose between, and why the quality of the document matters so much. Then the 18-step process makes a lot more sense.

What an annual report really is

An annual report is a company’s yearly account of its financial results, its statutory disclosures, and the story behind the numbers.

It has two halves. The statutory side carries the formal, required disclosures, including the Management Discussion and Analysis. The non-statutory side carries the narrative and the visuals: the chairman’s message, the year in review, and the sections that show what the company is really like.

The readers are a demanding group: investors, lenders, regulators, the board, and the analysts who follow the company. They do not read it for entertainment. They read it to judge how the year went and where things are heading, which is why both the numbers and the writing have to hold up.

An annual report is built from two halves that run in parallel and meet near the end.

Annual report or integrated report?

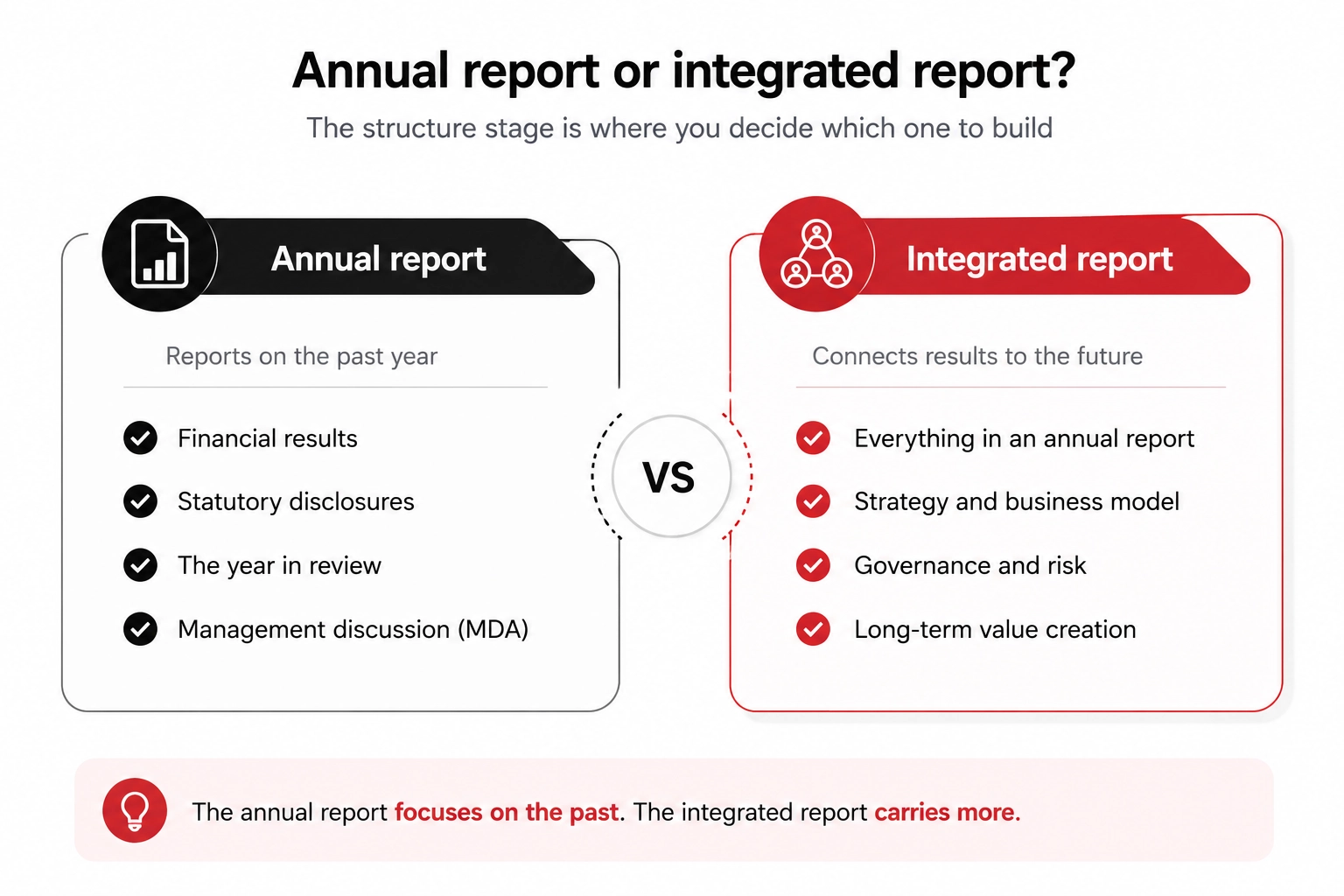

An annual report reports on the past year’s financial and statutory performance, while an integrated report goes further and links that performance to strategy, governance, and long-term value.

The annual report answers what happened this year. The integrated report answers what it means for the years ahead, connecting the financial results to the business model, the risks, and how the company builds value over time.

Which one you need depends on your reporting obligations and the story you want to tell. The decision is made early, when the structure is mapped, because it changes which sections the report has to carry.

The two report types share a base, but the integrated report carries more.

Why a strong annual report is worth the effort

A strong annual report builds confidence in the company, while a weak one quietly costs it credibility with the people who matter most.

Investors and analysts often turn to the MDA before they look at anything else. If that section is thin, or the report is hard to follow, it raises a quiet doubt about how carefully the company is run. The document is read as a signal, not just a record.

This is also why the fire-drill approach is so costly. A report thrown together in the final two weeks shows it: rushed writing, charts that do not match, and errors that slip through. The reader may not name the problem, but they feel it.

The answer is not more effort at the end. It is a real process that starts early and runs in order. That is what the rest of this post walks through.

The four teams behind every annual report

An annual report is built by four teams working in sequence: Research, Editorial, Design, and Production.

Research gathers the data and writes the heavy content, including the Management Discussion and Analysis. Editorial shapes the theme and proofreads the writing. Design turns the brand and the content into finished pages. Production prepares the section templates, lays out the statutory pages, and produces the final print-ready file.

Four teams, each owning part of the report, are working on one shared timeline.

Most reports go wrong when these four are kept apart: a separate writer, a separate designer, and a separate printer who never speak to each other. When they sit on one timeline, the writing and the design stay aligned from the first day instead of being forced together at the end.

How the 18 steps fit together

The 18 steps fall into four phases: setting the direction, building the design foundation, writing the structure and content, and then designing, reviewing, and printing.

Seeing the whole map first makes the detail easier to follow. The early phases are about agreement and direction. The middle is where the research and writing happen. The last phase is where everything is designed, checked, and turned into a finished file.

The full process: 18 steps across four teams, grouped into four phases.

Here are the 18 steps in the order they happen.

Step 1: Kick-off meeting

The process starts with a kick-off meeting, not a design brief.

This brings the report team and the company’s interfacing team together to agree on two things: the theme direction and the overall structure of the report. It is also where the company shares its brief for the coverline or theme and raises any timeline concerns at the outset.

Skipping it is where most delays begin. If the structure is not agreed upon early, every later stage gets reopened, and a planned project turns into a scramble.

Step 2: Theme ideation and concept finalisation

Next, the editorial team brainstorms and shares theme options, and one is chosen as the concept for the report.

The chosen theme is not decoration. It becomes the guiding idea, the North Star, that every later decision is checked against: the cover, the section openers, and the tone of the writing. Pick it well, and the report feels like one connected piece. Pick it loosely, and it reads like unrelated sections bound together.

Step 3: Understanding the brand guideline, image collection,n and standardisation

Before any design begins, the team studies the company’s brand guidelines and standardises its images.

This keeps the report consistent with everything else the company publishes, so it reads as part of the brand rather than a separate document. Collecting and standardising the images now also saves rework later, when the pages are laid out.

Step 4: Cover design options and finalisation

With the brand understood and the theme locked, cover options are designed and one is finalised.

The cover comes this early for a reason. It sets the visual language for the whole report: the dividers, the section openers, and the colour treatment all follow from it. Because the cover depends on the theme, step 2 has to be settled first, or the cover gets redone twice.

Step 5: Defining the reporting structure

The report’s structure is then mapped around the company’s operations and the type of report it needs.

This is the point where the annual-or-integrated decision becomes real. Sections are added to match the business and the reporting type, so a manufacturer and a financial services firm do not get the same skeleton. Defining it now gives the writing and design teams a clear shape to build toward.

Step 6: Data collection through research interviews and questionnaires

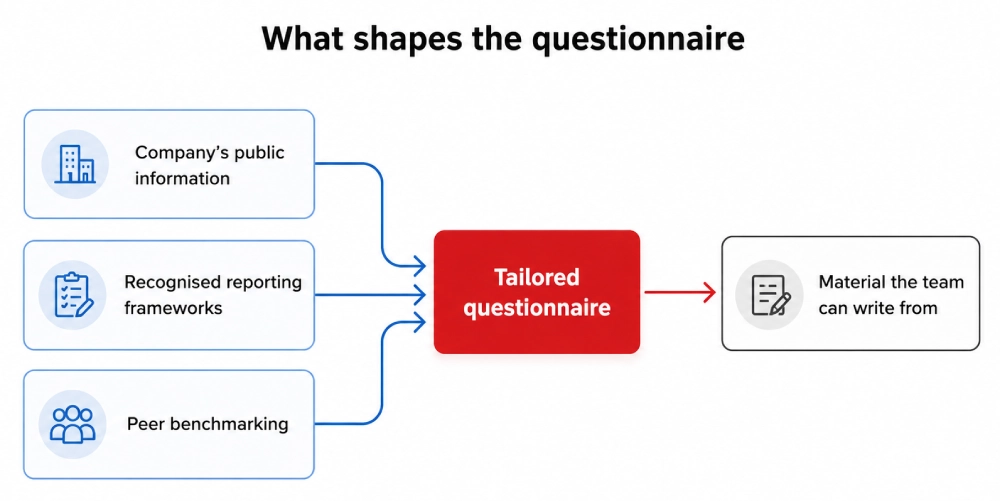

The content comes from structured research: interviews and a tailored questionnaire, not a generic form.

The questionnaire is built around the agreed structure and shaped by three inputs: the company’s public information, recognised reporting frameworks, and a look at how peer companies report. This is where reports are won or lost, because it gives the writing team real material instead of vague notes.

Three inputs shape the questionnaire that the writing team works from.

Step 7: Draft the Management Discussion and Analysis (MDA) section

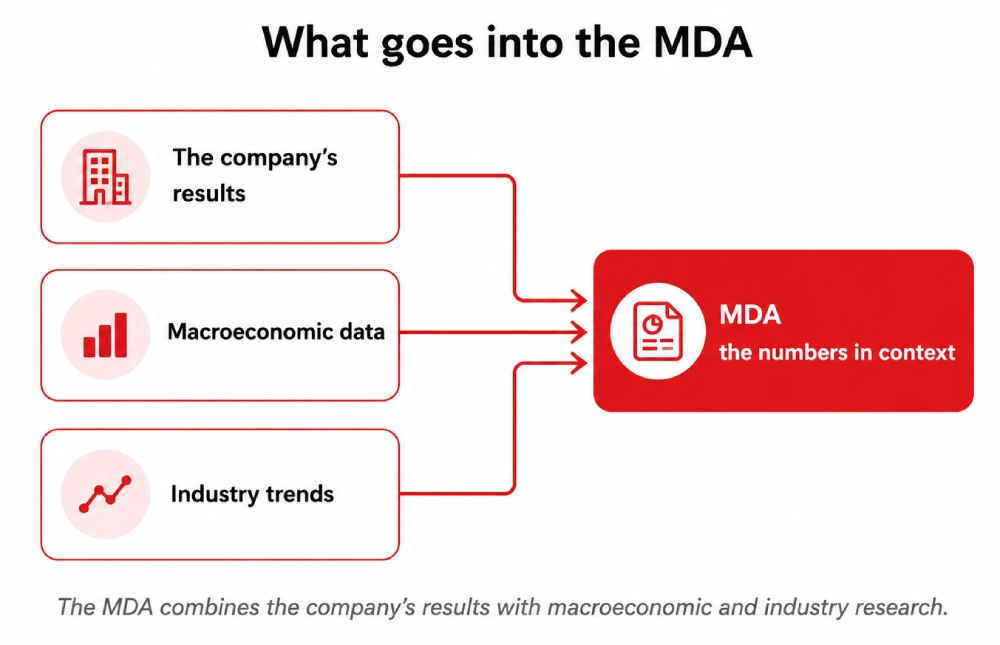

The Management Discussion and Analysis, or MDA, is drafted next, and it carries more weight than almost any other part of the report.

Investors and analysts often read it first. It is where the numbers get their context: why revenue moved the way it did, what the market did, and where the company sees things heading. The research team drafts it against macroeconomic data and industry trends, so the analysis rests on more than internal opinion.

The MDA combines the company’s results with macroeconomic and industry research.

Step 8: Drafting the non-statutory (initial pages/coloured pages) section

Alongside the MDA, the non-statutory pages are drafted: the opening and coloured sections that carry the company’s story.

These are the pages most readers see first: the chairman’s message, the year in review, and the people and culture sections. They are written from the interview and questionnaire inputs gathered in step 6, which is why that research step matters so much.

Step 9: Second cut of the MDA section

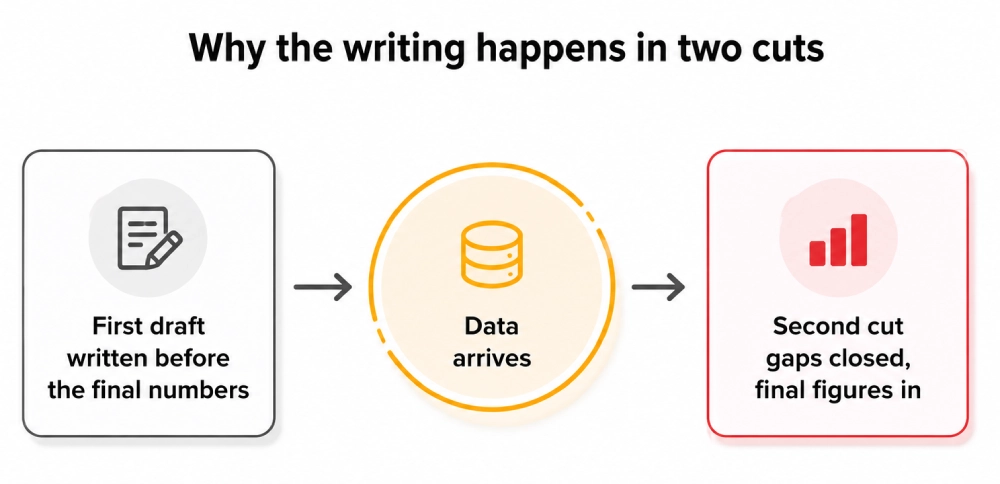

The MDA is then written a second time, revised against the data that has since arrived.

The first draft is written before all the numbers are final. The second cut closes the gaps and tightens the analysis once the real figures are confirmed. Writing in two passes lets the work start early instead of waiting for every last number.

The same two-cut cycle applies to the MDA and the narrative pages.

Step 10: Second cut of non-stat section

The non-statutory pages get the same treatment: a second cut with the final quantitative figures plugged in.

By now, the narrative is in place and the confirmed numbers slot into it. This is the difference between a report drafted calmly over weeks and one crammed into the final days.

Step 11: Template options for the statutory section

While the narrative is being prepared, the production team builds template options for the statutory section.

These templates are built from the brand guidelines and the cover design, so the formal pages match the rest of the report. Running this in parallel with the non-statutory work is what keeps the timeline manageable.

Step 12: Non-stat design

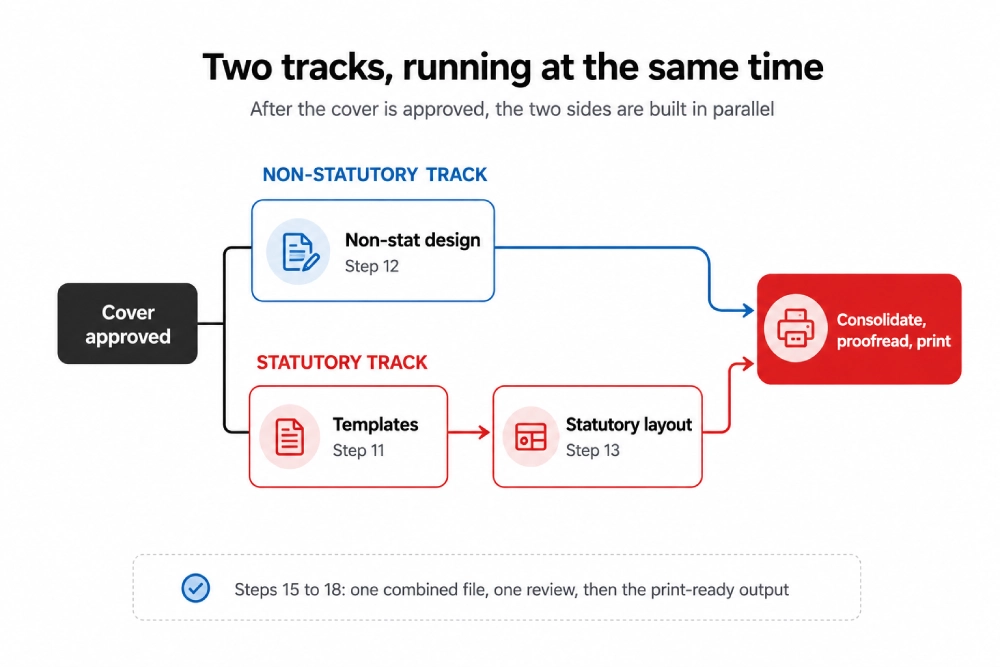

The non-statutory narrative pages are designed once the cover direction is approved.

This is where the drafted story becomes finished pages. The approval gate matters: the design waits for the cover, so the team does not build pages that later have to be scrapped.

Step 13: Layout of the statutory section

The statutory section, including the MDA, is laid out after its template is signed off.

With both tracks now in design, the two halves of the report, the story and the disclosures, come together at the same pace. The diagram below shows how the two tracks run in parallel and then merge.

With the cover approved, the two tracks run in parallel and merge for the final review.

Step 14: Corrections/feedback

Feedback is then applied section by section, and each section is finalised.

Handling corrections per section keeps them clean, rather than chasing changes across the whole document. Each section is closed out before the report is assembled.

Step 15: Consolidated file for review

All the sections are combined into a single file for a full review.

This is the first time the report is seen as one continuous piece, from the cover to the back page. It catches the problems that only show up when everything sits together: a tone that drifts, a chart style that changes halfway, or a section that runs too long.

Step 16: Proofreading of the non-stat and MDA section

The whole report is then proofread for grammar, consistency, and standardisation.

This is a dedicated stage, not a quick read-through. A report can be well written section by section and still be inconsistent across the whole: two spellings of one term, numbers formatted three ways, headings that do not match. A proper proofread standardises all of it.

Step 17: Final version before print

After the company’s final approval, the upload-ready version is produced with final quality checks.

This is the version fit to publish online. The final checks confirm that nothing slipped during consolidation and that every approved change is in place.

Step 18: Print-ready file

Finally, the print-ready file is prepared within three to four working days of final approval.

It is a fast finish, but only because the discipline came earlier. The agreed structure, the second cuts, the approval gates, and the proofread are what make the final stretch calm instead of frantic.

What a disciplined process actually buys you

An annual report is not really a design task or a writing task. It is a project, and like any project, the result depends on the order of the work.

The 18 steps come down to a few simple ideas: agree on the direction before you build, research before you write, write in two passes so data gaps do not derail you, run the statutory and non-statutory sides in parallel, and review the whole thing as one piece before it prints.

Companies that follow a process like this stop treating the annual report as a yearly emergency. The report reads better, the numbers carry their context, and the year-end is calmer for everyone involved.

If you would rather hand the whole thing to a team that runs this process every day, our annual report design service covers all 18 steps, from the kick-off meeting to the print-ready file.

Frequently Asked Questions

What is an annual report?

An annual report is a company’s yearly account of its financial results, its statutory disclosures, and the story behind the numbers, published for investors, lenders, regulators, and other readers.

It combines two sides: the statutory disclosures, such as the audited financial statements and the Management Discussion and Analysis, and the non-statutory narrative, such as the chairman’s message and the year in review.

How is an annual report made?

An annual report is made through a staged process that moves from a kick-off meeting and theme, through structure and research, into writing, design, review, and a final print-ready file.

In practice, it runs across four teams, research, editorial, design, and production, with the statutory and non-statutory sections built on parallel tracks and brought together for a single review before print.

What are the main sections of an annual report?

The main sections of an annual report are the financial statements, the Directors’ Report, the Management Discussion and Analysis, the corporate governance and statutory disclosures, and the narrative pages such as the chairman’s message and the year in review.

For larger Indian listed companies, the report also includes a Business Responsibility and Sustainability Report (BRSR).

How long does it take to produce an annual report?

A full annual report takes several weeks of structured work, with the print-ready file prepared within three to four working days of final approval.

The overall timeline depends on how ready the company’s data is and how many revision rounds the content needs. The process is built to start the writing early, so the final stretch stays short.

What is the MDA section in an annual report?

The Management Discussion and Analysis, or MDA, is the section where management explains the year’s financial results, the conditions behind them, and the outlook ahead, in plain narrative rather than only numbers.

It usually covers the industry and economy, business performance, financial position, risks, and internal controls, giving readers the context behind the figures. The research team drafts it against macroeconomic data and industry trends, which is why investors often read it first.

Is the MDA section mandatory for Indian companies?

Yes. For listed companies in India, SEBI’s Listing Obligations and Disclosure Requirements (LODR) require the annual report to include a Management Discussion and Analysis, either within the Directors’ Report or as an addition to it.

It typically covers industry structure, business performance, financial condition, risks, and internal control systems, along with a cautionary note on forward-looking statements.

What is the difference between an annual report and an integrated report?

An annual report focuses on the past year’s financial and statutory performance, while an integrated report also links that performance to strategy, governance, and how the company builds value over the short, medium, and long term.

The right choice depends on a company’s reporting obligations and the story it wants to tell that year.

Is integrated reporting mandatory in India?

Integrated reporting is voluntary in India. SEBI has advised the top 500 listed companies by market value to adopt it, but it is not a legal requirement.

Companies that do adopt it can present it as a separate chapter in the annual report, within the MDA, or as a standalone report, and may host it on their website.

What is the difference between the statutory and non-statutory sections?

The statutory section carries the formal disclosures a company is required to publish, including the financial statements and the MDA, while the non-statutory section carries the narrative and visuals, such as the chairman’s message and the year in review.

In a well-run process, the two are built on parallel tracks and consolidated for a single review before print.

Who prepares a company’s annual report?

A company’s annual report is prepared jointly by its internal team-, usually finance, the company secretary, and investor relations- and an external design and content partner that handles the writing, design, and production.

Internally, the finance team owns the numbers, and the company secretary owns the statutory disclosures. A reporting partner turns that material into a written, designed, and print-ready document.

What is the difference between an annual report and financial statements?

Financial statements are the audited numbers, such as the balance sheet, profit and loss account, and cash flow statement, while an annual report is the full document that contains those statements plus the narrative, the MDA, and the statutory disclosures.

In other words, the financial statements are one part of the annual report, not the whole thing.

Should an annual report be printed or digital?

Most companies now produce both a print-ready annual report and a digital version, because different readers prefer different formats.

A digital or interactive PDF is easy to share and host online, while a printed copy is still expected at annual general meetings and for key investors. Many Indian companies host the report on their website and circulate a digital copy with the AGM notice.

What makes a good annual report?

A good annual report is accurate, easy to read, and consistent, with the numbers given clear context and the design carrying the company’s brand from the cover to the back page.

The strongest reports treat the MDA as a real explanation rather than a formality, keep the writing plain, and read as one connected piece instead of separate sections stitched together.

Why is research so important in annual report preparation?

Research gives the writer real material to work with. A tailored questionnaire, peer benchmarking, and public filings turn vague inputs into specific, accurate content.

That is what makes a report feel specific to the company rather than read like a generic template.